As the old saying goes, “bla bla bla, death and taxes”.

It’s that time of the year where tax payments are due, yay! Hong Kong’s method of computing salary-based taxes based on Actual Year of Assessment (i.e. the year you worked) PLUS the following Provisional Year of Assessment (one more year in the future) is pretty brutal, especially when you’re expected to pay the computed taxes for both years pretty much upfront.

This is especially painful if you’re in your second year of working in Hong Kong as you need to pay the full tax amount for both assessed years. The first thing is to understand how the Inland Revenue Department (“IRD”) computes these taxes in the first place so you can start planning the best ways to maximise your tax allowances and deductions throughout the year. A good place to start would be IRD’s website which is chock-full of information, but absolutely worth your time to go through.

However, the focus of this post is on what you can do once the tax assessment is finalised, i.e. when the taxman rings your doorbell to cough up the goods.

Step 1 – Apply For Paying Tax By Instalments

Generally you would receive your Tax Notice around the second half of the year, which will inform you to make payments in 2 instalments, once in January and then again in April. The amount payable across the both instalments may vary for each taxpayer, principally the first instalment is the balance of the final tax payable (if any) plus 75% of the provisional tax due. The second instalment is the remaining 25% of the provisional tax due.

Thus, unless you’re a jet-setting CEO making bank, you should consider applying to IRD to further stretch out your tax payments, with the general conceit being that you may encounter difficulties making these big lump sum payments and need assistance to stagger the payments more to alleviate the impact on managing your cashflow. My application was successful and I managed to get my tax payments split equally across 6 months, but my friends have received tax payment terms as long as 12 months, so the outcome isn’t binary.

Disclaimer : By applying, you may be subject to further penalties (generally ranging from 5% to 10%) if you do not repay your taxes in time.

Additionally, there will be a transient 5% surcharge on the remaining tax payments due, which will be reduced after every payment you make.

Alright, let’s delve into the details below.

The Application Process

The first step is to submit your application form. There are several ways to do this:

- By fax (who uses fax machines anymore??)

- By post

- In-person

- Online (recommended)

You can find out more on the application process by visiting IRD’s website here.

Step 2 – Paying Your Tax Bill

The key channels you can pay your tax bills are:

- In Person

- By Post

- By Phone

- Online (recommended)

In Person

There are 3 main ways to pay in person. They are:

- Post Office

- Convenience Stores (7-Eleven, Circle K, VanGO, U Select)

- ATM’s

All of them have various functions including paying in cash, EPS (using your ATM debit card), and cheques. However, they are relatively inconvenient (e.g. HK$5,000 cash limit per transaction in convenience stores) and there is no additional value to extract from these payment options, so I won’t be elaborating further.

By Post

By Phone

Find out more on their website here.

Online

- Bill Payment feature on most bank websites/apps

- Faster Payment Systems (FPS)

- Electronic Tax Reserve Certificates (ETRC)

- E-cheque (more relevant for businesses)

Bill Payment

The Bill Payment feature exists for most Hong Kong bank apps, and as the name states this feature can be used to pay all kinds of bills or invoices by various organisations in Hong Kong. Notably, many of the government bodies are usually accessible, including Inland Revenue Department.

Depending on whether you have a bank account and/or a credit card with the bank, you can usually use either to pay off your bills without additional fees. Through this process you can manually key in the amount you would like to pay, which helps if you have limited funds in your account or credit balance. Either way, you make payment by inputting the Shroff Account Number that is present in your Tax Notice and Instalment Payment Voucher(s).

I recommend paying by credit card so you can stretch your tax payments by up to 2 months if you time it right (about a month to receive your credit card statement, and another month or so to make payment). That being said, I’m quite sure most credit cards do not give rebates or points for bill payments to government bodies, so if you are maxing out your credit limit, do take into consideration the opportunity cost of using the credit card on making a purchase that actually earns you points.

To clarify, I recommend that you pay off the full amount of your credit card statement so that you do not incur any penalties or interest, which will easily wipe out any explicit or implicit gains you may get from using your credit card.

You may consider using the Mox Credit card, see my previous post here.

Faster Payment System (FPS)

FPS is a great way to transfer funds and is available to all banks and digital wallets in Hong Kong. In most cases, all you need is someone’s mobile number or e-mail address to send funds to them. For companies, they usually have a unique FPS ID that you can input in your bank/digital wallet app. For IRD specifically, you will need to use your bank/e-wallet app to scan the QR code in your Instalment Payment Voucher(s). Thereafter, just verify that the right payee and amount is displayed (you cannot modify the amount for most banks) and complete payment.

Electronic Tax Reserve Certificates (ETRC)

ETRC’s are a unique way to squirrel away your funds into an account specifically created to pay your taxes. To buy ETRC’s you’ll need to submit an application form by post to IRD to open a TRC Account. When your account is opened, you can then start purchasing TRC’s which will be deposited into your account.

There are many ways to purchase TRC’s, notably using an autopay feature that some banks to automatically deposit funds into your account at your desired frequency. An interesting feature of the account is that it only pays you interest on your funds if you pay off your taxes with it. If you withdraw it for any other reason, you will not earn any interest. As of today the interest rate is at 0.925% p.a., which is actually better than most typical savings accounts. You can also turn on an “Auto Tax Payment Service” so you do not need to manually pay taxes on the due date. You can then pay the balance through other means.

Personally I will not use this function as I prefer managing my funds with less restrictions, and I am able to enjoy much higher interest rates by placing my funds in fixed deposits rather than the TRC account.

The Best Money Hack For Tax Payments (In January 2024)

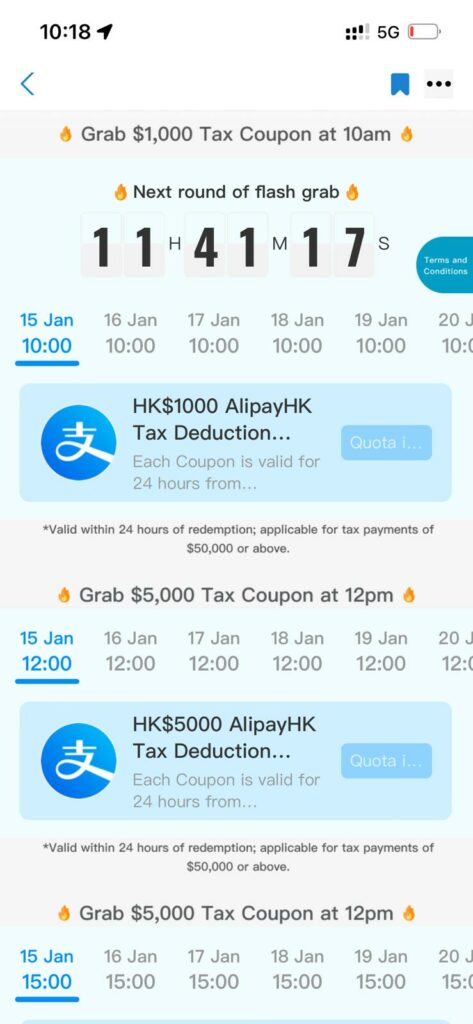

For now, AlipayHK seems to be dishing the more interesting tax deduction coupons which could go up as high as HK$5,000 off your tax bill (for tax payments of HK$50,000) or above. Needless to say, this is an incredible deal, BUT they only release the coupons once a day, and the quantity is severely limited. My feel is that they probably only release a handful everyday to entice you to come back often to try and get a coupon, but frankly you’ll need all the luck in the world to redeem it. Rather they have a more “generous” $50 coupon that is available every month for each account, which is similar to WeChat Pay HK.

Both apps allow you to earn their in-game currency which can then be used in many ways, usually to purchase a coupon for a subsequent transaction. While both apps have an earning rate of HK$1 : 1 for their in-app currency, by looking at the vanilla coupons that give a discount off a certain transaction, you generally get a discount of HK$1 for every 100 Wepoints (equivalent to 1% rebate) versus a discount of HK$1 for every 1,000 A. points (equivalent to 0.1% rebate).

The critical point to note, however, is AlipayHK allows you to use their points directly to offset any future transaction, but WeChat Pay HK requires you to purchase dollar coupons to offset any future transaction, and you can only use one coupon per transaction. As of today, the biggest e-cash coupon that WeChat Pay has is HK$50 (purchasable with 25,000 WePoints), thus if your bill payment is more than HK$50,000, you should use Alipay HK instead.

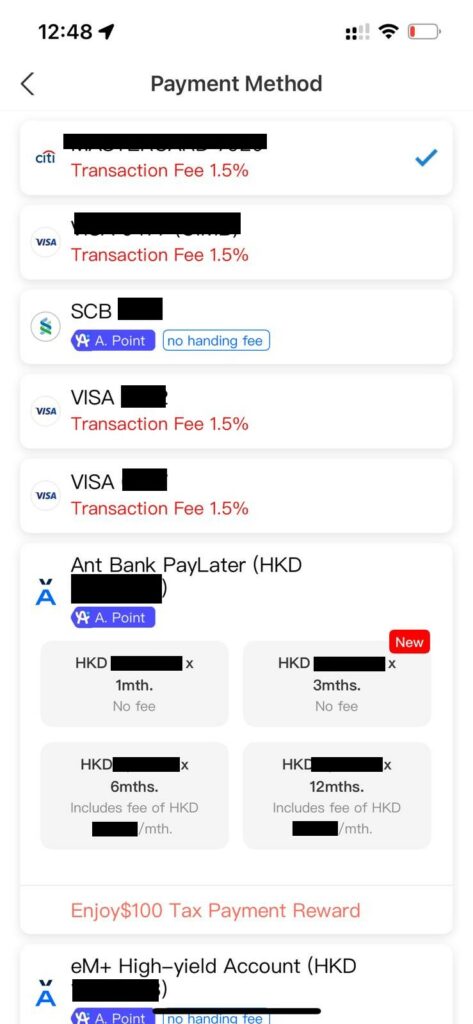

The kicker for me though, was the ability to combine the payment of my tax bill with Ant Bank’s PayLater scheme. Ant Bank is also owned by the same parent company as AlipayHK, Alibaba. Ant Bank PayLater allows you to further split your payment into instalments which range from 1 month to 12 months. At the moment, Ant Bank PayLater offers a 3-month instalment plan at no upfront fee and no interest fee. Assuming your tax bill is HK$50,000, with a 4% p.a. time deposit you could theoretically earn more than $300 on the cash float during these 3 months.

The cherry at the top is AlipayHK was giving out a HK$100 voucher for using Ant Bank’s PayLater service. All-in-all, I received HK$150 in deductions and rebates, and a further 0.1% of my payment in A. points which can be used to offset the next tax payment. You will need to open an Alipay HK account first by downloading the app, and then create an Ant Bank account (which is a virtual bank), and lastly apply for the PayLater scheme. There are numerous welcome gifts that AlipayHK and Ant Bank dish out, look out for them!

From the screenshot below, you can see paying with a credit card will incur a 1.5% transaction fee, and since most credit cards do not give points/rebates for payments made to WeChat Pay HK or AlipayHK, I would suggest paying with a bank account if you don’t have an Ant Bank PayLater account yet, as no fees are incurred and you can also earn A. points.

If you have found an even better way to pay your taxes, please comment and share below!