I became aware of the sim credit card a few months ago, and I only wish I heard about it earlier! It’s the maiden credit card offering of United Asia Finance Limited, a veritable financial institute that is one of the largest personal loan providers in Hong Kong. It’s a subsidiary of Sun Hung Kai & Co. Limited, one of several behemoth conglomerates in Hong Kong.

They are currently offering two types of credit cards:

- sim credit card; and

- sim World Mastercard.

The essential difference between the two is your annual income. You can apply for the World Mastercard version if you earn at least HK$150,000 per annum, otherwise you can apply for the sim credit card, including students. The cashback rates are the same for both cards, thus moving forward my post will treat both cards as one.

In general, I look for credit cards to maximise points earning or cash back based on these categories:

- Online spend;

- Offline spend; and

- Dining

- Retail (including supermarkets)

- All else spend (when the spend doesn’t quite fit in any of the first two categories)

- The Mox credit card falls under this category. Read my review here (opens new tab).

With that in mind, let’s see how the sim credit card fares in all 3 categories, but first, let’s look at their very attractive welcome offer.

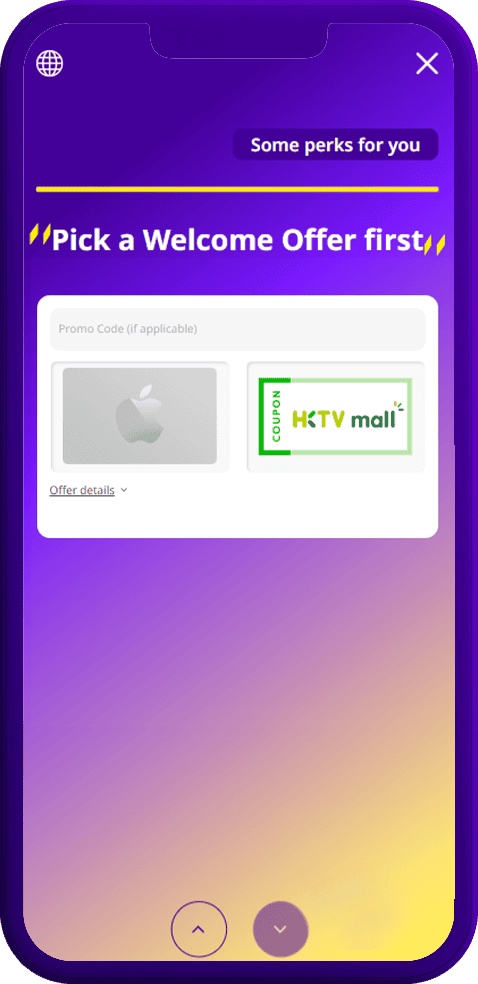

Welcome Offer

The Welcome Offer is pretty good, offering a choice of Apple gift vouchers or HKTVMall vouchers. For the sim credit card the reward is HK$500, and HK$1,000 for the World Mastercard.

The required eligible spend is HK$7,000 and HK$10,000 respectively within 60 days of card approval, meaning effectively you’re could be getting 10% value back on your spend, NOT including the usual cashback you’ll be earning from your spend, which means you could be earning as high as 16% value back in the form of vouchers and cashback!

Two big matters to take note for the welcome offer:

- If you’re maximising the cashback with online spend, note the online spend cap is HK$2,500 per calendar month (reasons explained below). Thus if you time your card application well, you could theoretically stretch your spend across 3 calendar months. This means to hit the HK$10,000 spend for the World Mastercard welcome offer, you will need to spend a further HK$2,500 (beyond the HK$7,500 for 3 calendar months) that will earn no cashback at all, hence the maximum value back at 16%; and

- The 60 days countdown starts at card approval, NOT at card activation (when you activate your physical card upon receiving it). I made the silly mistake of assuming the 60 days started when I activated the card (takes a few days for the card to arrive in your mailbox) and just missed out on meeting the spend requirement.

Online Spend

With a mouth-watering 8% cashback on online retail spend, the sim credit card blows its competitors out of the water, especially considering that the 8% cashback is not confined to any specific online category such as travel, food, transport etc. The next cashback card I have for online spend is at 6% (CNCBI Motion credit card), a significant 2% difference.

There are the usual exclusions in line with the general credit card company, such as:

- Transactions via an e-wallet (e.g. AlipayHK, WeChat Pay HK);

- Payments to government bodies (e.g. Inland Revenue Department), online bills and utilities bills;

- Payment of card fees or charges;

- Cash advances;

- Insurance-related payments;

- Charity donations;

- Finance-related transactions (e.g. buying unit trusts, casino transactions, money transfers etc.)

Online spend in other currencies are also eligible for the 8% cashback.

Offline Spend

The card also has 3% cashback for very specific retail transactions at 8 local merchants:

- Fashion/Sports

- Adidas

- Fila

- PUMA

- Reebok

- Cosmetics

- @cosme STORE

- Tokyo Lifestyle

- Matsumotokiyoshi

- Dining

- Sushiro

Beyond that, you will only be earning a paltry 0.4% cashback. Needless to say, keep your card in your wallet when spending at any other store!

Other Considerations

For many cashback cards, there is a cap of how much cashback can be received. The sim credit card has a hard cap of HK$200 combined across all spend. This means if you were to use it for online spend only, you should only spend at most HK$2,500. Anything beyond that will not earn you a single cent in cashback. Personally the cap is quite low relative to other cards, but it’s understandable given the high cashback rate. Thankfully, the card app displays transactions very clearly so it’s easy to keep track of your spend.

The cashback is calculated on calendar month basis, so plan your spend well, but please take note that there’s usually some delay between your transaction date and when it gets posted in your credit card statement. As with many cards, any cash back or points earning calculation is based on the posting dates of the transaction, meaning if you were to transact on 31 January and it gets posted on 1 February, then the cashback will calculate this transaction for the month of February.

The Annual Fee for the principal card is HK$1,800 and HK$800 for the World Mastercard and sim credit card respectively. The supplementary cards are HK$900 and HK$400 respectively. While the Terms & Conditions are silent on waiving of the annual fee for the first year, I was not charged the annual fee when my card was approved, and I suspect that’s the intention otherwise it would have been dead on arrival. As always, be sure to set a reminder to call sim to waive the annual fee when it’s due! Personally I haven’t reached the 1-year mark with my card, but since I’m maxing out the cashback spend cap every month, I hope that should be sufficient to get a waiver.

Pros and Cons

Here’s what I like and dislike about this card:

Pros

- Best cashback (8%) for online spend for any local card;

- Very attractive welcome offer that provides 10% value back on the spend requirement;

- Decent cashback (3%) for 8 local merchants; and

- Simple and quick sign-up process on app or website (Elaborated in subsequent sections).

Cons

- Abysmal 0.4% cashback for any other offline spend;

- Low cashback cap at HK$2,500 for online spend (I recommend keeping this card for online spend only);

- Hard cashback cap, meaning additional spend beyond the threshold earns no rewards, unlike other cards which may offer some low earn rate;

- No auto payment setup possible yet, meaning you need to pay your bills manually. It’s not a big issue, but I’m personally juggling at least 10 credit cards so handling bills gets very cumbersome if I have to remember which cards need to be repaid manually; and

- Potential end to the super high cashback soon. The current promotion is valid until 30 April 2024. It’s unclear if sim intends to continue offering the same cashback rate, but since this is their inaugural launch promotion, I have an uneasy feeling they will bring down the cashback rate pretty significantly, especially if they have met their sign-up targets. As they say, make hay while the sun shines!

Sign-Up Process

Signing up was a very easy process, especially once you’ve applied for a few credit cards. The usual documents you require are:

- HKID;

- Payslips (past 3 months) [optional if you’re a student]; and

- Proof of address (e.g. bank statements, utility bills etc.)

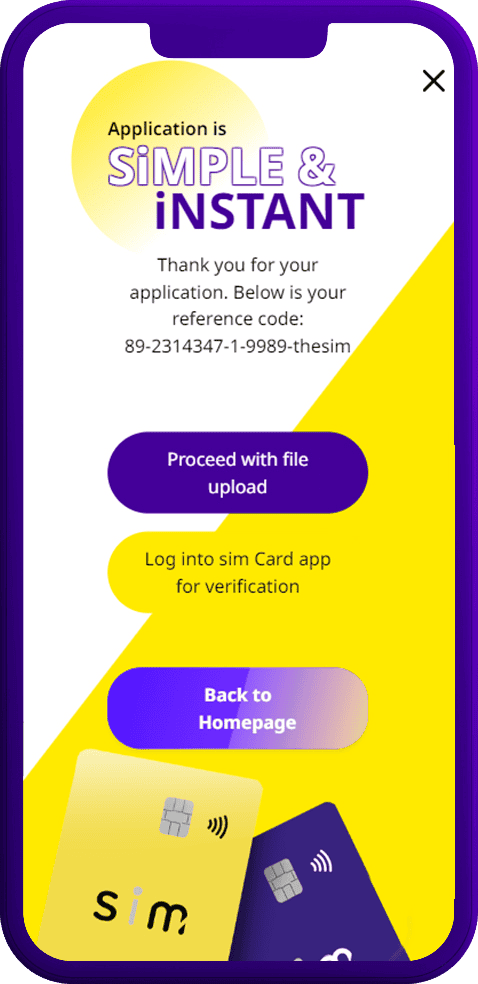

It only takes 3 main steps to complete your application.

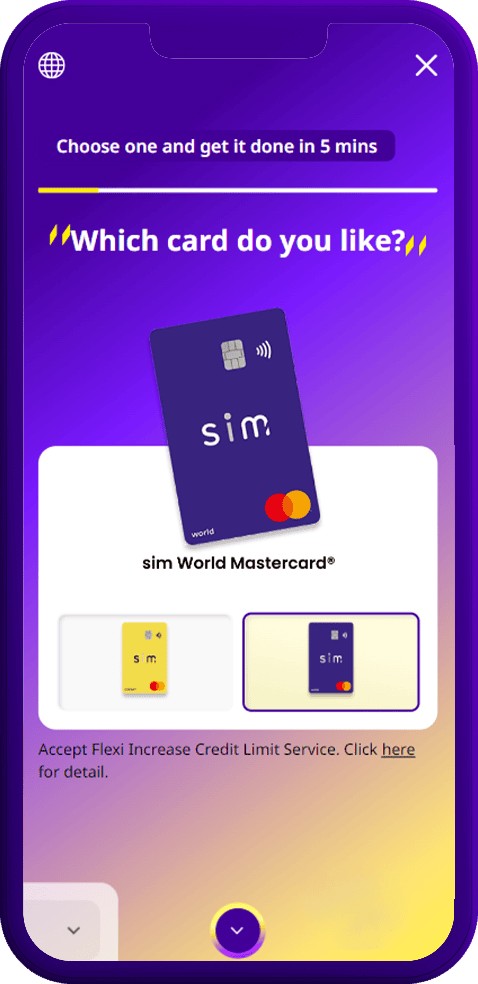

Step 1 : Choose your card

Step 2: Fill up your information and upload documents

Step 3 : Choose your Welcome Offer

The process is equally convenient on the website or on their app.

Source: sim credit card app

Conclusion

I love this card, and as long as they maintain the 8% online spend cashback, it will continue to stay in my wallet. That’s a big if though, let’s see what comes after when the current promotion ends on 30 April 2024.

This card also serves as one of the major credit cards that I use to pay my rent and get some sweet cash back! Look out for more details in a future post.

To find out more, visit their website here (opens a new tab).